24. November 2018

/

/

Archiv

Opinion: The Eurozone’s fiscal rules no longer work for Italy

10 min Lesezeit

ZAC TATE

Editor’s note: this is the first opinion piece published by Dezernat Zukunft. It will be our practice to identify opinion pieces clearly, and to accompany them with links to one or more pieces that defend different or opposing judgements. We hope that this will help to stimulate productive discussion. For this piece, we recommend readers to also look at Blanchard, Leandro, Merler and Zettelmeyer’s piece for PIIE, arguing that “Italy’s budget is unlikely to stimulate growth and may well depress it”, and as a consequence “Italy would have fared better with a roughly fiscally neutral budget”; and Guntram Wolff’s short piece at Bruegel, arguing that priority should be given to improving the effectiveness of public investment and the productivity of small service sector firms, rather than boosting aggregate demand.

“If Italy wants special treatment, that would mean the end of the euro. So you have to be very strict.”

Those were the words of EU Commissioner Jean-Claude Juncker, reflecting on the Italian government’s draft budget for 2019. The worry behind Juncker’s remarks, of course, was that Italy could become the new Greece, with a populist government running up unsustainable debts, eventually forcing the Eurozone into a choice between either bailing out Italy or facing the spillover effects of a messy default—a choice sure to renew tensions between Northern and Southern Europe and to imperil the single currency.

While this danger is real, there is an equal and opposite one: by preventing an elected government from meeting its electoral promises, the EU could play into the hands of those who call for the country to leave the euro, ultimately undermining both the political cohesion and geopolitical power of the European Union. This risk becomes clear when one sees how the EU’s fiscal rules not only severely restrict Italy’s policy freedom but are also self-defeating in their outcomes.

Italy is in a rut

Measured per capita, Italy has seen next to no economic growth since 1999—a fact that is particularly striking when compared to growth of roughly 15-25% in Germany, France and Spain over the same period. In the Mezzogiorno, unemployment remains close to 20%.

The euro is not the only cause of Italy’s poor performance. Levels of university education are too low; businesses specialize too much in traditional, low-growth activities; and national banks have lent recklessly. Italy is also burdened by large amounts of legacy public debt, built up in the 1970s and 1980s, that restrict more recent governments’ scope for investment.

However, neither can Italy’s poor growth record be explained without reference to the euro: in the 1980s, to meet the requirements of the European Monetary System (the precursor to the euro), the Bank of Italy clamped down on high inflation by steeply raising interest rates, stopped directly funding public borrowing, and started issuing bonds to the private sector instead. This sharply increased the public debt and the costs of servicing it.

The inability of Italy to issue currency and the Eurozone’s body of rules place further constraints on Italy. The conservative, low-inflation bias of the European Central Bank (ECB), combined with weak productivity growth in Italy, has meant that the country has had to keep its own inflation rate close to zero in recent years to maintain competitiveness with countries such as Germany. This prevented its real debt burden from decreasing gradually through steady, low, inflation, and suppressed business activity as a result.

As a result Italy’s public debt to GDP ratio, currently at over 130%, has grown by 15% since 2010, even though the country has spent less than it raises in taxes every year since 2009. This combination of low growth, balanced primary budgets, and nevertheless rising debt levels has proven politically unsustainable, with the Italian electorate electing to office parties that promised, in breach of Eurozone rules, to spend more and boost the economy.

A mandate for breaking rules, albeit with uncertain consequences

Following their election victories, the 5 Star and Lega parties negotiated and signed a coalition government built around spending plans amounting to an increase of €125 billion a year (or 7% of GDP). This reflected their popular mandate but ran up against two problems.

First, the plans were a clear breach of the EU’s Fiscal Compact rules, which state that countries cannot run a budget deficit of more than 3% of GDP. If a country nevertheless insists on doing so, it forfeits the right to assistance from the European Stability Mechanism and the ECB in times of crisis.

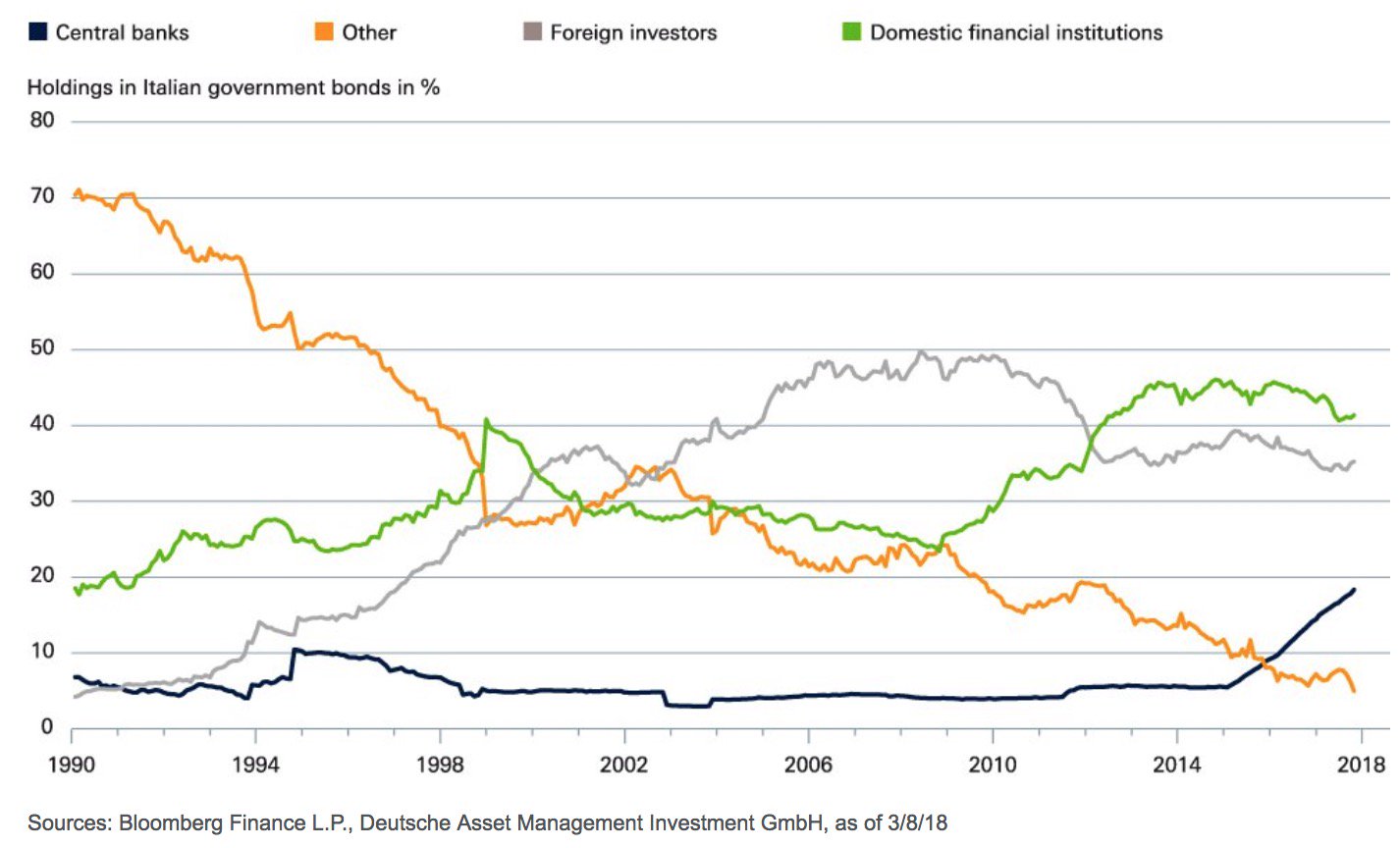

Second, in December 2018 the ECB is ending its bond-buying programme. This matters greatly for Italy since, for the last three years, the ECB was the only net buyer of Italian government bonds. From next year on, Italy will need to rely almost entirely on private markets to buy any new bonds it issues to fund its promises.[1] Currently, foreign investors and domestic banks together hold 75% of Italian debt, while Italian households hold less than 10%.

That means that unless Italian households are willing to absorb the new debt, the state may have to pay higher interest rates to fund its budget. Driving up both government borrowing costs and those of businesses and citizens throughout the economy, Italy’s public debt might then quickly look precarious. If this leads any of the banks holding Italian debt to become themselves weaker, it might trigger another economic crisis. That is the principal concern of the European Commission, which worries about cross-border systemic risks.

Changing the rules

The government has since significantly scaled back its spending plans, aiming at a 2.4% deficit for next year. While this moves within the EU’s three-percent overall deficit limit, it still breaks the club’s rules on structural deficits, which for Italy are set at 0.5% of GDP per year.

Although structural economic reforms are needed in Italy, we have learned since 2008 that these are best embedded in a context of strong aggregate demand. Insofar as the EU’s fiscal rules prevent the government of Italy from creating this demand, and insofar as the German government—together with other governments with the fiscal space to do so—chooses not to provide it, the rules of the Eurozone prevent the government of Italy from creating the economic (as well as the political) conditions in which structural reforms can succeed.

In addition, a number of growth-enhancing reforms—in particular those related to infrastructure investment, education spending, and re-training of the workforce—require, in their very nature, significant spending. If these are to go ahead, they must either be financed from higher taxes—not impossible, but both politically challenging and, unless raised mostly from high incomes, potentially aggravating Italy’s lack of aggregate demand—or from additional borrowing. In restricting the use of the latter, Eurozone rules hence not only prevent the creation of a reform-conducive macroeconomic context, but also render the implementation of directly growth-enhancing reforms harder than it need be.

Both of these point towards changing the rules. A number of northern European countries, including Germany, the Netherlands and Ireland, however, are reluctant to move beyond the current rules. Northern Europe is particularly allergic to what Angela Merkel calls a ‘debt union’—the likely result of a pan-European deposit insurance, mutual debt guarantees, or large and direct fiscal transfers between countries.

While there are good reasons why Northern European states should feel reluctant to assume liability for debts that Italy built up during the 1970s and 1980s, there remains the problem that the eurozone’s rules do not meet the interests of one of its largest members. As outlined above, years of spending restraint have not reduced Italy’s public debt burden, even as economic growth remains tepid, skilled young people emigrate, support for the populist parties strengthens, and support for the euro slides. This is primarily a problem for Italy, but creditor countries, too, have a stake in its solution: should Italy leave the Euro, the currency will appreciate, rendering German exports less competitive globally, and German-owned assets abroad (outside the Eurozone) less valuable.

There is a solution that restores a fair balance. The EU should allow Italy to moderately breach the Fiscal Compact and increase spending, but request that Italy use the funds only for investment purposes that raise the country’s growth potential. If Italy were willing to accept oversight, the EU should mutualise the debt to keep borrowing costs low. The rules governing the ECB should also change, allowing for higher inflation that would give states with greater debt burdens more space to invest. Steps in this direction would strengthen the Eurozone and tackle deeper issues and imbalances within Europe’s political economy.

This is because such a deal not only maintains limits on Italy’s sovereignty; it also imposes restrictions on other countries such as Germany, whose export sector currently benefits disproportionally from low inflation and generates too much surplus capital, much of which ends up—due to both public and private unwillingness to invest in Germany—in Southern Europe. Such a deal also recognises the responsibilities that interdependent nations have to each other and acknowledges, as John Maynard Keynes first noted, that creditors in a monetary union always have the greater ability to adjust, even as if they, unlike debtors, can choose whether or not they want to.

Finally, this deal would also pay heed to the fact that free market competition does not lead to an automatic equalization of living standards across the different regions of an economy. Instead, left to themselves, firms and workers tend to congregate in already existing clusters of high-value add activity, for example in Southern and South-Western Germany or Northern Italy, which thus pull further ahead of other regions.[2] If approximately equal living standards are a basic political commitment,[3] then the results of the “new trade theory” imply as necessary either permanent transfer payments from high- to low-value-add regions, or active state intervention to prevent the ever greater concentration of high-value add activities around existing clusters, or a mixture of the first and the second.

A more flexible Europe

And here lies the wider point. So long as Europeans continue to attach importance to their national identities—and surveys suggest that they overwhelmingly do—the EU will continue to have to deal with what German philosopher G.W.F Hegel called the “particular wills” of each nation, shaped by their unique historical experiences and evolving understandings of their own interests. This means that a particular framework of international rules that provides stability at one point in time can become a source of instability at a later point in time. The belief that any one particular set of common European rules is the right one for all time is, seen against this background, a dangerous fiction. It will inevitably conflict with the evolving interests and dynamics that continually shift just below the surface.

In the absence of a European demos, there is hence no alternative to the EU evolving, one crisis at a time, whenever the existing set of rules stops working for everyone. This is not a sign of failure. It does mean, however, that we cannot be dogmatic about existing rules. Instead, we must be alive to the real and diverse lived experiences of Europe’s citizens of different nationalities, willing to build a set of flexible and fair political institutions, and able to change course without calling into question the fundamentals of our Union.

Negotiating the Italian budget, in other words, is not about giving special favours, as Jean-Claude Junker claims, but about flexibly adjusting the operation of European rules, thereby maintaining consent and legitimacy for the European project. Being ‘very strict’ cannot always be the answer.

Picture credit: Caribb, under CC BY-NC-ND 2.0

[1] Since the ECB may choose to reinvest monies that it receives in repayment of the bonds that it currently holds, it may continue to be a buyer of Italian government bonds, though it is unclear to what extent, if any, it would continue to be a net buyer.

[2] This is the key result of the “new trade theory” launched by Paul Krugman in the 1990s.

[3] This is the case, for example, in the German Constitution.

Hat dir der Artikel gefallen?

Teile unsere Inhalte

{kind=link}

{kind=link}