Dollar dependence is becoming costly, China is a useful case study in reducing it

- The US is increasingly willing to weaponise the dollar, turning the world's dominant currency into an instrument of geopolitical pressure

- China is the most instructive case of a major economy trying to loosen its dollar dependence. Its record shows what is achievable and where progress is difficult.

China achieved asymmetric success

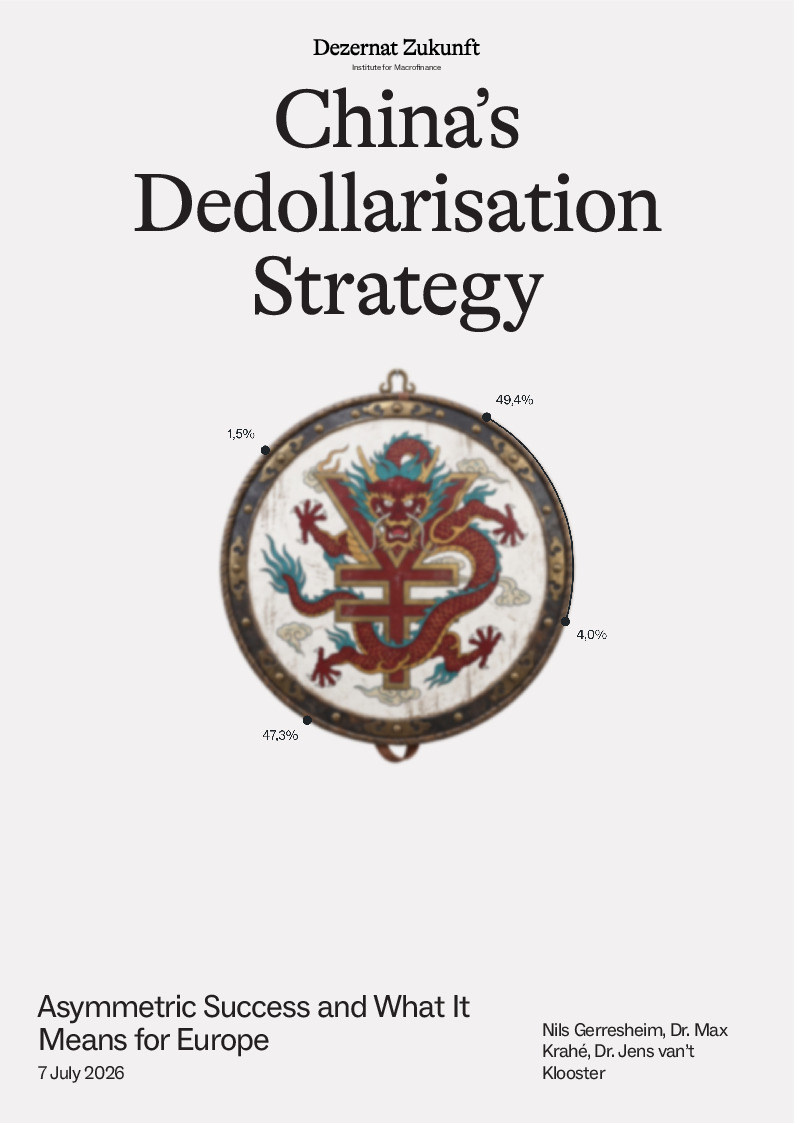

- An international currency is used for three purposes — settlement, invoicing, and investment.

- China has cut dollar dependence mainly in settlement: more than half of its trade now settles in RMB, up from 10 percent in 2012. This was achieved through providing efficient payment infrastructure.

- Invoicing and investment remain dollar-bound. RMB invoicing is rare, the currency is barely used between third countries, and China still holds a large stock of dollar reserves and assets.

- Capital controls are the binding constraint. Without deep, open, and liquid RMB markets, FX-hedging stays costly and the deeper use-cases cannot follow settlement. Lifting these controls would force China to give up either exchange-rate management or monetary sovereignty, a trade-off Beijing has been unwilling to make.

- China may nonetheless have achieved an important aim: without opening its financial system, it has largely insulated itself from US payment sanctions. Exclusion from the dollar system would no longer isolate China the way it initially did Russia or Iran.

Two Lessons for Europe

- Europe is similarly, if not more, exposed to the dollar. European investors hold roughly USD 3 tn in US Treasuries and some USD 9 tn in long-term US securities, and European banks intermediate large volumes of dollar funding.

- Efficient payment infrastructure can reduce reliance on dollar settlement, Europe's most exploitable dependency. This opportunity should be seized.

- Reducing invoicing and investment dependence may be easier for Europe than for China: Europe has open capital markets, China does not. Increasing safe asset volumes and liquidity would be key.

- But reducing invoicing and investment dependencies may be a lower priority. Sanctioning European assets imposes costs on the US Government that are difficult for the Federal Reserve to manage. This makes it a less credible threat.

- Nonetheless, the July 2025 EU-US trade deal illustrated the US Government’s willingness to engage in brinkmanship. The riskiest path may be to do nothing.